Understanding the fundamental accounting concepts of increases and decreases in account balances. The distinction between these concepts is crucial for accurate financial record-keeping and analysis.

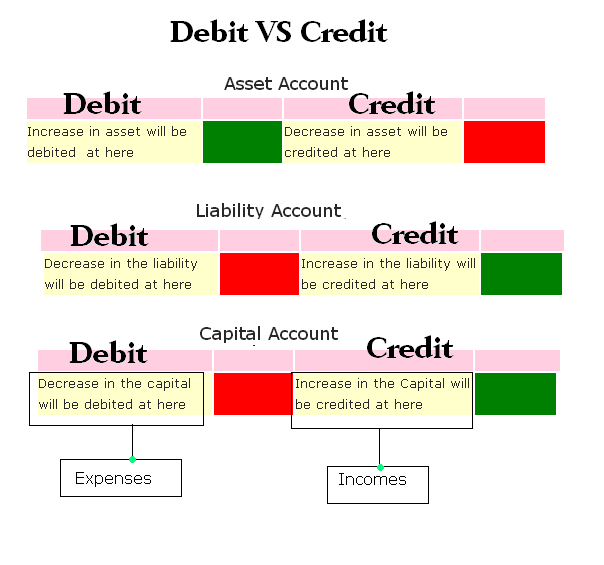

Increases and decreases in account balances are fundamental to accounting. A credit increases the balance of some accounts and decreases the balance of others. Conversely, a debit decreases the balance of some accounts and increases the balance of others. This seemingly simple distinction has significant implications for the accuracy and reliability of financial statements. For instance, a credit to a liability account increases the amount owed by the business, while a debit to the same account decreases the amount owed. Similarly, a credit to a revenue account increases the amount earned by the business, while a debit to the same account decreases the amount earned. A crucial aspect of understanding this is recognizing which accounts are affected by debits and credits. Proper application of these principles is fundamental to maintaining a consistent and accurate record of financial transactions.

The importance of correctly applying these concepts stems from the core function of accounting: to provide a true and fair view of a company's financial position. Accurate recording of transactions ensures that financial statementssuch as balance sheets and income statementsreflect the actual state of affairs. Incorrect application of debits and credits can lead to inaccurate reporting, potentially misleading stakeholders and impacting decision-making processes. Furthermore, consistent application of these principles across all transactions is necessary for comparability and analysis over time, enabling a business to track its financial performance and make informed projections. Internal controls and audit procedures depend heavily on the meticulous application of these principles to ensure financial data integrity.

Moving forward, the detailed application of these principles will be examined, along with specific examples to illustrate their practical use.

credit vs debit

Understanding the distinction between credit and debit is fundamental to accurate financial record-keeping. These terms represent opposing effects on account balances, essential for creating reliable financial statements.

- Account balance

- Transaction impact

- Increased values

- Decreased values

- Double-entry system

- Financial reporting

The concepts of credit and debit are inextricably linked. Credit increases certain accounts (like revenue or liabilities) and decreases others (like equity or assets). Conversely, debit decreases certain accounts (like revenue or liabilities) and increases others (like assets or expenses). This interplay is integral to the double-entry bookkeeping system, where every transaction affects at least two accounts. Understanding these effects is crucial for producing accurate financial statements, like balance sheets and income statements, and for effective financial analysis. For example, a sale (increasing revenue) would be recorded with a credit to the revenue account and a debit to the cash account. Proper application ensures a consistent and accurate record of financial transactions, crucial for informed business decisions and reliable financial reporting.

1. Account balance

Account balance represents the difference between total credits and total debits for a specific account. This difference is fundamental to understanding a company's financial position and activity. The relationship between account balances and the concepts of credit and debit is direct and crucial for accurate financial reporting.

- Impact of Credits and Debits

Credits increase certain account balances (e.g., revenue, liability accounts) and decrease others (e.g., assets, equity accounts). Debits have the opposite effect; they decrease certain accounts (e.g., revenue, liability accounts) and increase others (e.g., assets, equity accounts). Understanding these opposing effects is essential for determining the net change to an account and, subsequently, the account balance. Proper application of these effects is vital for accurate bookkeeping. Incorrect application can lead to distorted account balances, hindering accurate financial statements and impairing informed decision-making.

- Maintenance of Accuracy

The double-entry bookkeeping system relies on the principle of equal debits and credits for every transaction. Maintaining this balance is critical for accurate account balances. Any discrepancy signifies a mistake in the recording process, demanding immediate correction. Systematic, consistent application of credit and debit rules ensures accuracy in account balance calculations. Anomalies in account balances suggest errors in recording, posting, or processing, necessitating investigation.

- Financial Statement Reflection

Account balances directly influence the preparation of financial statements, such as the balance sheet and income statement. The balance sheet, for example, reflects the company's assets, liabilities, and equity at a specific point in time. The values for these components are derived from the balances of the respective accounts. This connection makes account balance management crucial for accurate and reliable financial reporting and analysis. An accurate balance sheet is essential for evaluating a company's financial health.

- Analysis and Interpretation

Account balances provide essential data for financial analysis. Trends in balances across different periods offer insights into a company's financial performance and position. Comparison of account balances to industry benchmarks or previous periods helps in assessing overall financial health and identifying areas requiring attention. For example, consistent increases in the balance of accounts receivable may suggest difficulty collecting payment from clients. Such analysis is vital for evaluating a company's financial position and performance, enabling informed strategies for improvement.

In conclusion, the interplay between account balances, debits, and credits is fundamental to sound financial record-keeping. Maintaining accurate account balances is essential for producing reliable financial statements and enabling effective financial analysis, which drives crucial business decisions and fosters sustainable growth.

2. Transaction Impact

Every financial transaction has a direct impact on a company's accounts. This impact is meticulously documented using the principles of credit and debit. A transaction's effect, whether increasing or decreasing an account balance, is categorized as either a credit or a debit. This categorization is fundamental to the double-entry bookkeeping system. Understanding this connection is crucial for accurate financial record-keeping and for producing reliable financial statements. For instance, a sale increases cash and decreases inventory. This change is reflected in the accounts by a debit to cash and a credit to inventory. Conversely, if a company pays salaries, cash decreases and expense increases. This is documented with a debit to expense and a credit to cash. These examples highlight how transaction impact directly determines the use of credit and debit, ensuring consistency and accuracy.

The practical significance of understanding this connection is substantial. Accurate recording is vital for decision-making, enabling management to monitor financial performance, identify trends, and make informed strategic choices. Misunderstanding this relationship can lead to inaccurate financial reporting, potentially misleading stakeholders and compromising the reliability of financial data. For example, if a purchase is incorrectly recorded, it will impact inventory, accounts payable, and potentially cost of goods sold, leading to incorrect profit calculations. This error has ripple effects throughout the financial statements, creating a distorted view of the company's financial health. This highlights the critical importance of meticulously tracking every transaction's impact, utilizing correct debits and credits, to maintain a transparent and accurate record.

In conclusion, the impact of every financial transaction is fundamental to the credit and debit system. This intricate connection is a core component of the double-entry bookkeeping system, vital for producing accurate financial statements. Precise recording of transaction impacts, using appropriate credits and debits, is essential for informed decision-making and the overall financial health of a company. Without this understanding, financial information becomes unreliable, potentially leading to misjudgments and negative consequences.

3. Increased Values

Increased values in accounting are directly linked to the concepts of credit and debit. Understanding how these increases are reflected through debits and credits is crucial for accurate financial reporting and analysis. This connection is fundamental to the double-entry bookkeeping system, where every transaction impacts multiple accounts and must be precisely recorded.

- Impact on Specific Accounts

Certain accounts are inherently linked to increases. For instance, an increase in assets (like cash, inventory, or equipment) is typically reflected by a debit. Conversely, an increase in liabilities (like accounts payable or loans) or equity (like retained earnings or owner's equity) is usually recorded with a credit. Recognition of these specific account relationships is paramount for maintaining the integrity and accuracy of financial records. Revenue increases are also typically recorded with a credit.

- Transaction-Specific Analysis

The specific transaction dictates how an increase manifests. A sale, for example, leads to an increase in revenue (recorded as a credit) and cash (recorded as a debit). The recording reflects a simultaneous increase in two distinct accounts. Similarly, receiving a loan increases cash (debit) and increases the liability (credit). Carefully analyzing the nature of the transaction is essential for correctly applying credits and debits. A meticulous understanding of transaction impacts is critical for maintaining accurate records of financial changes.

- Accuracy in Financial Statements

Accurate reflection of increased values through correct application of credits and debits ensures reliability of financial statements. A balance sheet, for example, requires accurate representations of asset increases and decreases. Similarly, income statements rely on precise recordings of revenue increases. The integrity of these statements directly hinges on the correct use of credits and debits to represent increased values. Misapplication leads to inaccuracies, affecting stakeholder perception and hindering informed decision-making.

- Maintenance of Accounting Equation Balance

The accounting equation (Assets = Liabilities + Equity) must always balance. Increased assets, liabilities, or equity are interconnected. A rise in one component necessitates offsetting changes in other components, reflected by credits and debits. Any imbalance reflects an error that must be identified and corrected to maintain the accuracy of the overall financial picture. Proper treatment of increased values is critical to maintain the fundamental integrity of the accounting equation.

In summary, increased values are central to the credit-debit system. Correctly identifying and recording these increases is vital for generating reliable financial statements. Accuracy in this area ensures that financial records accurately reflect a company's financial position and performance, leading to better decision-making based on accurate data. Maintaining this accuracy is crucial for stakeholders and the sustainability of a business. The proper allocation of credits and debits is pivotal for accurate record-keeping of increases in various accounts, ensuring the integrity of financial information.

4. Decreased Values

Decreased values in accounting represent reductions in account balances. These reductions, critical components of the credit-debit system, are meticulously recorded to maintain accurate financial statements. The connection between decreased values and the distinction between credit and debit is direct and consequential. Understanding this interplay is vital for precise financial reporting and analysis. For instance, a decrease in inventory is reflected by a credit to the inventory account and a debit to the related cost of goods sold account, simultaneously affecting two or more accounts.

The impact of decreased values extends beyond mere bookkeeping. Correctly recording decreases in assets like inventory or cash, and decreases in liabilities, equity or expense, is essential for presenting an accurate financial picture. Inaccurate recording leads to misstatements in financial reports, potentially misleading stakeholders. For example, if a company fails to appropriately record a decrease in accounts receivable (customers not paying), the company's financial position appears healthier than it actually is. This misrepresentation can lead to poor investment decisions or inappropriate financial strategies. Properly acknowledging decreases, using appropriate debits and credits, safeguards the integrity of financial information. The consistent application of these principles is vital for long-term financial health and for building trust with investors and stakeholders. A decrease in retained earnings from dividends paid out is another example, affecting both the retained earnings and cash accounts. The appropriate credit and debit entries are essential to maintain accurate financial records.

In summary, decreased values, when correctly accounted for using the credit-debit system, are integral to producing reliable financial statements. Accurate recording of decreases is vital for a truthful representation of a company's financial performance and position. Such accuracy fosters transparency, facilitates informed decision-making, and builds trust among stakeholders. The avoidance of errors in recording decreases, utilizing appropriate credit and debit entries, is crucial for the integrity of financial reporting and, subsequently, for a company's overall success.

5. Double-entry system

The double-entry system is intrinsically linked to the concepts of credit and debit. This system forms the bedrock of accurate financial record-keeping. Its fundamental principle mandates that every transaction affects at least two accounts, with the sum of debits always equaling the sum of credits. This equality ensures the integrity of the accounting equation (Assets = Liabilities + Equity). The application of credit and debit is a direct consequence of this system. A sale, for example, increases cash (debit) and simultaneously increases revenue (credit). This double-entry approach maintains the balance of the accounting equation, crucial for a precise representation of financial position and performance.

The double-entry system's importance stems from its inherent ability to maintain this balance. Any transaction, regardless of complexity, necessitates a corresponding debit and credit entry. This meticulous record-keeping is paramount for the accuracy of financial reports and analysis. Consider a purchase of inventory. The debit would be recorded to inventory (increasing its value) and the corresponding credit to accounts payable (increasing the company's obligation). The balance remains intact, preserving the accuracy of all related accounts. The integrity of the system ensures financial statements accurately reflect a company's financial status, enabling informed decisions and reliable reporting for stakeholders.

In essence, the double-entry system provides a structured framework for applying credits and debits. It ensures every transaction is accurately reflected in the accounting records. The interconnectedness of debits and credits within this system is critical. Without the double-entry system, the application of credit and debit would be arbitrary and potentially lead to inaccuracies, jeopardizing the reliability of financial reports and decisions. This highlights the vital role the system plays in maintaining a truthful and consistent portrayal of financial activity, facilitating effective decision-making and stakeholder confidence.

6. Financial Reporting

Accurate financial reporting is fundamentally reliant on the correct application of credit and debit principles. The integrity of financial statements, including balance sheets, income statements, and cash flow statements, hinges on meticulous record-keeping using these opposing accounting entries. Maintaining consistency in the use of debits and credits ensures a true and fair view of a company's financial position, performance, and cash flows, vital for stakeholders' decision-making.

- Balance Sheet Accuracy

The balance sheet, reflecting a company's financial position at a specific time, is directly affected by the use of credits and debits. Correctly applying these principles ensures that assets, liabilities, and equity are accurately represented. For example, an increase in inventory (an asset) is reflected by a debit to the inventory account. Conversely, an increase in accounts payable (a liability) is shown by a credit to the accounts payable account. Inaccurate use of these entries leads to a misrepresentation of the company's financial standing, potentially misleading investors and creditors.

- Income Statement Reliability

The income statement, summarizing a company's financial performance over a period, heavily depends on the correct application of credits and debits for revenue and expenses. Accurate recording of revenue through credits and expenses through debits is crucial for determining net income. Errors in this application can distort profitability figures, affecting the perception of a company's operational efficiency and potentially influencing investment decisions. A sale, for example, increases revenue (credit) and cash (debit), showcasing the interplay of credit and debit in generating income statement data.

- Cash Flow Statement Consistency

The cash flow statement tracks the movement of cash inflows and outflows. The appropriate use of credits and debits reflects the flow of cash in various activities operating, investing, and financing. For instance, receiving cash from a customer results in a debit to cash and a credit to accounts receivable. Conversely, paying an employee's salary results in a debit to salary expense and a credit to cash. Accuracy in these entries is crucial for accurately portraying the company's cash management capabilities and its ability to generate and utilize cash.

- Auditing and Compliance

Financial reporting practices must adhere to established accounting standards (e.g., Generally Accepted Accounting Principles - GAAP or International Financial Reporting Standards - IFRS). Consistent use of credit and debit ensures compliance with these standards. Auditors rely on the meticulous application of credit and debit principles for auditing financial statements. Accurate recording and appropriate use of debits and credits is essential to avoid inaccuracies that could compromise compliance with reporting standards and regulatory requirements. Errors can result in penalties and legal ramifications.

In conclusion, the meticulous use of credit and debit in financial reporting is fundamental to the creation of accurate and reliable financial statements. The interconnectedness of these accounting principles with various financial statements underscores their critical role in conveying a precise picture of a company's financial health to stakeholders. This accurate portrayal of financial performance and position is pivotal for investors, creditors, and managers to make informed decisions. Any deviation from these standards can distort financial reporting, potentially jeopardizing the integrity and value of financial information.

Frequently Asked Questions

This section addresses common queries regarding the fundamental accounting concepts of credit and debit. Clear answers to these questions aim to clarify the application of these principles in financial record-keeping.

Question 1: What is the fundamental difference between a credit and a debit?

A credit increases the balance of some accounts (e.g., revenue, liabilities) and decreases the balance of others (e.g., assets, equity). Conversely, a debit decreases the balance of some accounts (e.g., revenue, liabilities) and increases the balance of others (e.g., assets, equity). The crucial distinction lies in the effect on different account types, not a singular increase or decrease.

Question 2: Why is the double-entry system essential to credit and debit?

The double-entry system is essential because it mandates that every transaction affects at least two accounts. This ensures the balance of the accounting equation (Assets = Liabilities + Equity) is maintained. Correct application of debits and credits within this system is vital for accurate financial reporting.

Question 3: How do credits and debits impact the balance sheet?

Credits and debits directly affect the balance sheet by changing the balances of asset, liability, and equity accounts. For example, a credit to accounts payable increases the liability side of the balance sheet. Conversely, a debit to cash increases the asset side. Correct application maintains the balance sheet's accuracy.

Question 4: How do credits and debits relate to increases and decreases in account balances?

The relationship is not one-to-one. A credit increases certain accounts (like revenue or liabilities) while decreasing others (like assets or equity). A debit decreases some accounts (like revenue or liabilities) and increases others (like assets or equity). Understanding the specific impact on each account type is essential.

Question 5: What are potential consequences of misapplying credit and debit principles?

Misapplication can result in inaccurate financial statements, leading to flawed analyses and potentially misleading stakeholders. This can affect investment decisions, creditworthiness assessments, and the overall perception of the organization's financial health. Misapplication necessitates a thorough review and correction to restore accuracy.

Understanding the nuances of credit and debit is vital for maintaining accurate financial records. These principles underpin all financial reporting and are foundational to effective financial analysis. Correct application ensures reliability and transparency, enabling informed decision-making for all stakeholders.

This concludes the FAQ section. The next section will delve into specific accounting transactions and their treatment using debits and credits.

Conclusion

The exploration of credit and debit reveals their fundamental role in accurate financial record-keeping. The principles of credit and debit, when applied correctly, underpin the double-entry bookkeeping system, ensuring the integrity of financial statements. This system dictates that every financial transaction affects at least two accounts, with the sum of debits always equaling the sum of credits. This crucial balance maintains the integrity of the accounting equation (Assets = Liabilities + Equity). Understanding how credits and debits impact different account types increasing some and decreasing others is essential for accurate financial reporting. The interplay of these concepts in various financial statements, including balance sheets, income statements, and cash flow statements, is critical for a true and fair representation of an entity's financial position and performance.

Accurate application of credit and debit principles is not merely a technical exercise; it is fundamental to sound financial management. Precise recording using these principles facilitates informed decision-making, enabling stakeholders to assess financial health, evaluate performance, and project future outcomes. Maintaining this accuracy is critical to building trust in financial reports and promoting responsible financial practices. The meticulous application of these fundamental principles directly impacts the long-term viability and success of any organization.

You Might Also Like

Gabriel's 90 Day Fianc Journey: Love & Challenges!Candace Cameron Bure's Husband - Who Is Valeri Bure?

Fiji Radio Mirchi: Listen Now!

Rachel Gatina: Top Stories & Insights

Jason Momoa & Dwayne Johnson: Epic Duo Or Friendly Rivalry?

Article Recommendations

- George Sakellaris Inspiring Stories Insights

- 1955 Quarter Value How Much Is Your Coin Worth

- Michael Marchetti Top Insights Strategies