Understanding the fundamental concepts of debits and credits is essential for anyone working with accounting. This knowledge forms the bedrock of double-entry bookkeeping systems, impacting financial reporting and decision-making.

Debits and credits are the two fundamental accounting entries. They are used to record transactions in a double-entry bookkeeping system. The core principle is that every transaction affects at least two accounts. A debit increases the balance of some accounts, while decreasing the balance of others. Conversely, a credit increases the balance of some accounts, while decreasing the balance of others. Crucially, the total debits must always equal the total credits. This ensures the accuracy and integrity of the accounting records. For example, if a company purchases office supplies for cash, the Cash account will be debited (reflecting a decrease in cash) and the Office Supplies account will be credited (reflecting an increase in the value of supplies). This double-entry ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced.

The importance of this system lies in its ability to provide a comprehensive and accurate representation of a company's financial position. This detailed record allows for informed decision-making, effective financial planning, and accurate reporting to stakeholders. By ensuring a balance between debits and credits, companies gain a clear view of their assets, liabilities, and equity, which are fundamental components of financial statements like the balance sheet. The system's longevity underscores its crucial role in financial integrity and accountability.

Moving forward, we will delve into specific examples of how debits and credits apply to various accounts, such as assets, liabilities, equity, revenues, and expenses, illustrating their impact on the financial statements.

Difference Between Debit and Credit in Accounting

Understanding the distinction between debits and credits is fundamental to accurate financial record-keeping. This system, crucial for double-entry bookkeeping, ensures financial statements accurately reflect a company's financial position.

- Increase asset accounts

- Decrease liability accounts

- Decrease equity accounts

- Increase expense accounts

- Decrease revenue accounts

- Debit left side

- Credit right side

- Balance equality

These aspects highlight the directional impact of debits and credits on various account types. For example, a debit increases the balance of an asset account (e.g., cash) while decreasing the balance of an expense account (e.g., salaries). Conversely, a credit increases the balance of a liability account (e.g., accounts payable) and revenue accounts (e.g., sales). The fundamental principle of debit and credit ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced, providing a reliable basis for financial reporting and decision-making. This dual impact is vital for accurately reflecting financial transactions and maintaining the integrity of financial statements.

1. Increase Asset Accounts

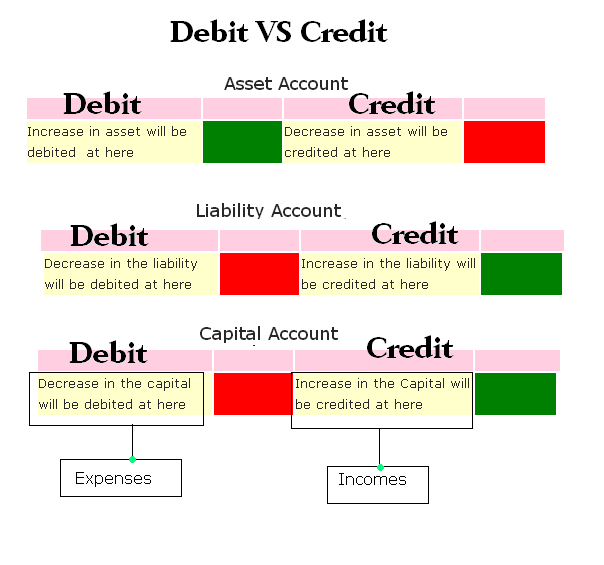

Increasing asset accounts is a key component of the debit and credit system in accounting. Assets represent a company's resources, such as cash, equipment, and inventory. An increase in an asset account necessitates a corresponding accounting entry, either a debit or a credit, depending on the nature of the transaction. For instance, if a company purchases equipment for cash, the equipment account increases (an asset), and the cash account decreases (also an asset). The accounting equationAssets = Liabilities + Equitymust remain balanced. Therefore, increasing an asset account requires a debit entry, which reflects the increase in value on the asset's side of the equation. The effect of this debit entry is balanced by a corresponding credit entry to another account, such as cash, reflecting the reduction in the cash account. This ensures the accuracy and integrity of financial records.

Consider a scenario where a company receives cash from a customer for services rendered. The cash account, an asset, increases. This increase is recorded as a debit to the cash account. Simultaneously, the revenue account (representing income earned) increases, which is recorded by a credit entry. The debit to cash balances the credit to revenue. This illustrates how a single transaction impacts multiple accounts while maintaining balance. Correctly identifying and recording these debits and credits is crucial for accurately reflecting the financial position and performance of the company. A systematic and accurate recording of increases in asset accounts ensures that financial statements reflect a realistic picture of the company's resources.

In summary, increasing asset accounts is intrinsically linked to the fundamental principle of debits and credits in accounting. Understanding the proper debit or credit entry is critical for maintaining the accuracy and balance of the accounting equation, providing a reliable basis for financial analysis and decision-making. This knowledge is essential for stakeholders, including investors, creditors, and management, as it directly impacts the reliability and credibility of financial reporting.

2. Decrease Liability Accounts

Decreasing liability accounts is a critical aspect of accounting, intricately linked to the fundamental principle of debits and credits. Liabilities represent a company's obligations to external parties, such as creditors or suppliers. Understanding how decreases in liabilities are recorded through debits and credits is essential for accurate financial reporting and decision-making.

- Impact on the Accounting Equation

Decreasing a liability account reduces the right-hand side of the accounting equation (Assets = Liabilities + Equity). A decrease in liabilities signifies that the company has settled obligations or reduced its outstanding debts. This directly affects the balance sheet and the overall financial position. For example, if a company pays off a loan, the liability account (loan payable) decreases. This decrease in liabilities results in a corresponding adjustment on the accounting equation.

- Debit Entries and the Double-Entry System

The double-entry bookkeeping system demands that every transaction have a corresponding debit and credit entry. When a liability account decreases, a debit entry is made to the liability account. This debit entry reduces the balance of the liability. Simultaneously, another account (often an asset account) is credited to reflect the effect of the transaction. For instance, if a company pays off accounts payable, the accounts payable account (liability) is debited, and the cash account (asset) is credited. The debit entry signifies the decrease in the liability, while the credit reflects the outflow of cash. This meticulous system ensures that the accounting equation remains balanced.

- Examples of Decreasing Liabilities

Various business transactions lead to decreases in liabilities. Payment of supplier invoices reduces accounts payable. Repaying loans decreases notes payable. Accrued interest payments decrease interest payable. Each instance involves a debit to the specific liability account and a corresponding credit to another account to maintain the balance of the equation. The consistent application of these principles assures financial accuracy and reliability.

- Importance for Financial Reporting

Accurate recording of liability decreases is crucial for preparing financial statements. Reporting reduced liabilities indicates improved financial health and efficiency. These reports provide stakeholders with a clear picture of the company's ability to meet its obligations. Investors, creditors, and management rely on this detailed information to evaluate financial performance and make strategic decisions.

In conclusion, the decrease in liability accounts, as reflected through debits and credits, is a pivotal aspect of the accounting process. This systematic recording ensures the accuracy and reliability of financial reports. By understanding the connection between these decreases and the accounting equation, businesses and stakeholders can make informed judgments about financial health and performance.

3. Decrease Equity Accounts

Decreasing equity accounts, a fundamental aspect of accounting, directly relates to the "difference between debit and credit." Equity represents the residual interest in the assets of an entity after deducting liabilities. A decrease in equity signifies a reduction in the owners' stake or a negative impact on the company's net worth. This decrease is reflected in the accounting equation (Assets = Liabilities + Equity) and necessitates a specific accounting treatment using debits and credits.

The decrease in equity is typically caused by various transactions, including expenses, dividends, or losses. For example, if a company incurs operating expenses, this reduces equity. The corresponding accounting entry involves a debit to the related expense account (reducing equity) and a credit to an account like cash or accounts payable (reflecting the outflow of resources). Similarly, when a company distributes dividends to shareholders, equity decreases, and the debit is made to the retained earnings account, while the credit goes to the cash account. A loss on the sale of assets also results in a decrease in equity. A loss account is debited, and the asset account is credited. These examples illustrate the consistent application of debits and credits to record changes in equity.

Understanding how decreases in equity are accounted for using debits and credits is vital for accurate financial reporting. This allows stakeholders to assess the financial health and performance of an entity. Inaccurate recording of these decreases can lead to skewed financial statements, misleading investors and creditors, and potentially impacting strategic decision-making. Consequently, a thorough understanding of the principles underpinning debits and credits is essential for ensuring the integrity and reliability of financial data. Properly recording these decreases in equity accounts, by adhering to the rules of debit and credit, safeguards the integrity of the accounting process, allowing for informed decision-making based on accurate financial representations.

4. Increase Expense Accounts

Increasing expense accounts is a crucial aspect of accounting, directly impacting the financial health of a company. Understanding how these increases are recorded, specifically through debits and credits, is fundamental to accurate financial reporting and analysis. The proper application of debits and credits in this context ensures the reliability of financial statements and facilitates informed decision-making.

- Impact on the Accounting Equation

Increasing expense accounts directly reduces equity, a component of the accounting equation (Assets = Liabilities + Equity). When a company incurs expenses, it utilizes resources, thereby decreasing its net worth. This reduction in equity is a direct consequence of the expense transaction. The debit entry reflects this decrease in equity. The double-entry system dictates that this debit entry must be balanced by a corresponding credit to another account, often cash or accounts payable, reflecting the outflow of resources related to the expense.

- Debit Entries and the Double-Entry System

Expenses are recorded with a debit entry. This debit increases the balance of the expense account. The double-entry bookkeeping system ensures that every transaction affects at least two accounts. A credit is made to another account to offset the debit entry, maintaining the balance of the accounting equation. For example, if a company pays salaries, the Salaries Expense account is debited, and the Cash or Accounts Payable account is credited. This reflects the decrease in cash or increase in accounts payable and balances the equation. This systematic recording process is crucial for accurate financial tracking and reporting.

- Examples of Expense Account Increases

Various business activities result in increases to expense accounts. Salaries, rent, utilities, and supplies are all examples of expenses. Each expense increase requires a debit to the corresponding expense account, mirroring the decrease in equity. The offsetting credit to another account ensures the integrity of the accounting records. Accurate and timely recording of these increases is vital for maintaining the reliability and transparency of financial reports.

- Importance for Financial Reporting

Detailed records of expense account increases are critical for preparing financial statements, particularly the income statement. This data provides insights into operational efficiency and cost management. A thorough understanding of these increases allows stakeholdersinvestors, creditors, and managementto assess a company's profitability and operating performance, leading to informed decision-making.

In conclusion, increasing expense accounts, properly recorded using debits and credits, is integral to maintaining accurate financial records. This aspect of accounting facilitates informed business decisions and helps stakeholders understand the financial health and performance of a company. A thorough grasp of this process is essential for producing reliable and insightful financial statements.

5. Decrease Revenue Accounts

Decreasing revenue accounts in accounting signifies a reduction in the inflow of resources generated from a company's core operations. This decrease, a critical component of the double-entry bookkeeping system, is meticulously tracked using debits and credits. A decline in revenue reflects various factors, including decreased sales volume, pricing adjustments, or a downturn in the market. Accurate accounting for such decreases is essential for a precise depiction of the company's financial performance. This process helps stakeholders understand the financial impact of these events.

The double-entry system necessitates that every transaction, including a decrease in revenue, must affect at least two accounts. When revenue decreases, a corresponding credit entry is made to the revenue account, reflecting the reduction. Concurrently, a debit entry is required in another account, often related to a factor causing the revenue decrease (e.g., a return of goods). This ensures the balance of the accounting equation (Assets = Liabilities + Equity) remains unchanged. For example, if a company grants a customer a return for unsatisfactory goods, the sales revenue account is credited (decreasing it), and a debit is made to an account such as a sales return account, or potentially inventory (depending on the specifics of the return). This maintains the equation's balance, providing a complete and accurate picture of the transaction's effect on the company's financial standing. Analysis of decreasing revenue trends assists in identifying potential issues or opportunities. Tracking these reductions against previous periods allows for meaningful comparisons and informed decisions about future strategies.

Understanding the connection between decreasing revenue accounts and the debit-credit system is vital for accurate financial reporting and analysis. A thorough grasp of this aspect facilitates informed decision-making, helping management assess the impact of various factors on a company's financial well-being. By maintaining a consistent and accurate record of these decreases, companies can ensure the validity and reliability of their financial statements, which are crucial for investors, creditors, and other stakeholders to make informed judgments about the company's financial health.

6. Debit Left Side

The placement of debits on the left side of an account is a fundamental aspect of double-entry bookkeeping. This convention, while seemingly arbitrary, is crucial to the "difference between debit and credit." It establishes a standardized method for recording transactions and ensuring the accuracy and integrity of financial records. The left-side location for debits isn't arbitrary; it facilitates the double-entry system, which requires every transaction to have a corresponding debit and credit. This system, deeply ingrained in accounting practices, guarantees that the accounting equation (Assets = Liabilities + Equity) remains balanced. The left-side placement for debits directly supports this crucial aspect of accounting.

The significance of this convention lies in its contribution to the overall integrity of the accounting process. For example, consider a company receiving cash from a customer. The Cash account, an asset account, increases. By debiting the Cash account, the increase is recorded on the left side, thereby reflecting the increase in the asset. Simultaneously, the corresponding credit entry is made to the account representing the increase, which in this example might be the Sales Revenue account. This placement of debits ensures accurate reflection of transactions within the accounting equation, ensuring the integrity of financial statements. Without this standardized placement, the system loses its precision and the accuracy of financial reporting is compromised. The debit on the left side acts as a clear indicator of the transaction's impact on the account, allowing for easy analysis and tracking.

In summary, the debit left-side convention is not merely a procedural detail. It is an essential component of the double-entry bookkeeping system. This standardized placement allows for accurate recording and balancing of transactions, ensuring the reliability of financial information. Without this consistent application, the fundamental principles of accounting would be significantly compromised, impacting the ability of stakeholders to make informed decisions. This seemingly simple convention is the bedrock of accurate financial reporting and analysis.

7. Credit Right Side

The placement of credits on the right side of an account is a fundamental aspect of double-entry bookkeeping. This convention, while seemingly arbitrary, is crucial to the distinction between debits and credits. It directly supports the fundamental double-entry system, a cornerstone of accounting. This system demands that each transaction have a corresponding debit and credit, ensuring the balance of the accounting equation (Assets = Liabilities + Equity). The right-side placement for credits directly supports this balancing act.

The significance of this convention lies in its contribution to the integrity of accounting. Consider a company selling goods on credit. The Accounts Receivable account, an asset, increases. A debit to the Accounts Receivable account reflects this increase. Simultaneously, revenue increases, requiring a credit to the revenue account. This credit entry reflects the increase in revenue on the right side, maintaining the balance. Without this consistent placement, the system's accuracy would be compromised. Each transaction, from recording a purchase to paying salaries, necessitates a corresponding debit and credit entry. The right-side placement of credits ensures these entries accurately reflect the transaction's effects on the accounting equation.

This consistent placement of credits on the right side of accounts provides a clear and concise way to track changes in various account types. From liabilities to equity, the right side of the account reflects increases in these categories. This standardized approach enables analysts and stakeholders to understand the effects of transactions. For instance, when recording a payment of salaries, cash (an asset) decreases, requiring a debit to the cash account. To maintain balance, a credit is made to the salary expense account on the right side, signaling the decrease in equity caused by the expense. This consistent system allows for clear analysis of financial performance over time, enabling critical decision-making and informed financial planning. In essence, the credit right-side convention facilitates the efficient and accurate recording of financial transactions, underpinning the reliability of financial reporting.

8. Balance Equality

Balance equality is a fundamental principle in double-entry bookkeeping. It dictates that for every transaction, the total debits must equal the total credits. This principle is inextricably linked to the difference between debits and credits, forming the bedrock of accurate financial record-keeping. Without this equality, the accounting equationAssets = Liabilities + Equitycannot remain balanced, leading to inaccurate financial statements. This principle ensures the integrity of financial reporting and provides a foundation for reliable financial analysis.

- Role in Maintaining the Accounting Equation

Balance equality is critical for maintaining the integrity of the accounting equation. Every transaction impacts at least two accounts. A debit to one account must always be matched by a corresponding credit to another. This ensures that the sum of debits always equals the sum of credits, preserving the balance of the equation. For example, if a company purchases equipment for cash, the debit to the equipment account (increasing assets) is balanced by a credit to the cash account (decreasing assets). This maintains the overall balance of the equation.

- Impact on Financial Statement Accuracy

Maintaining balance equality directly impacts the accuracy of financial statements. Inaccurate recording or failing to ensure debits equal credits can lead to misstatements in the balance sheet, income statement, and cash flow statement. This inaccurate representation of the company's financial position can mislead stakeholders, including investors and creditors, leading to potentially detrimental consequences. For example, if a company erroneously records a debit without a corresponding credit, the balance sheet will show an inflated asset value, creating a misleading picture of the company's financial health.

- Verification of Transaction Accuracy

Balance equality serves as a crucial check on the accuracy of recorded transactions. By ensuring debits and credits consistently balance, the system detects errors in recording. This verification function is paramount for preventing significant misstatements. For example, a discrepancy between debits and credits signals a possible error in the recording process, requiring immediate investigation and correction to maintain accurate records. This preventative measure safeguards against errors that can propagate through the entire accounting system.

- Basis for Financial Analysis and Decision-Making

The principle of balance equality provides a sound foundation for financial analysis and decision-making. Accurate financial statements, built on the principle of debits equaling credits, allow informed decisions about resource allocation, investment opportunities, and operational strategies. For instance, analyzing revenue and expense data on a balanced statement enables effective cost control and forecasting. This principle underpins efficient use of resources and facilitates successful financial planning and strategic development within a company.

In conclusion, the principle of balance equality is indispensable in accounting. It safeguards the accuracy of financial statements, enabling reliable financial analysis and sound decision-making. The connection between debits and credits, underpinned by the principle of equality, is fundamental to the integrity and reliability of financial reporting. The resulting consistent and accurate financial representation directly supports a multitude of decisions that drive the success or failure of a company.

Frequently Asked Questions about Debits and Credits in Accounting

This section addresses common questions regarding debits and credits, crucial components of double-entry bookkeeping. Understanding these concepts is essential for accurate financial record-keeping and informed decision-making.

Question 1: What is the fundamental difference between a debit and a credit?

A debit increases the balance of some accounts and decreases the balance of others, while a credit increases the balance of some accounts and decreases the balance of others. The key distinction lies in their impact on specific account types. The critical point is that for every transaction, the total debits must equal the total credits. This ensures the accuracy and integrity of the accounting records.

Question 2: How do debits and credits affect different account types (e.g., assets, liabilities, equity)?

The impact of debits and credits varies depending on the account type. For example, debits increase asset accounts and decrease liability accounts, while credits increase liability accounts and decrease asset accounts. Equity accounts are affected similarly, with debits often decreasing equity and credits increasing it. Understanding these specific impacts is crucial for correctly recording transactions.

Question 3: Why is the double-entry system crucial, and how do debits and credits contribute to it?

The double-entry system ensures accuracy by requiring a debit and a corresponding credit for every transaction. This linkage forces the equation Assets = Liabilities + Equity to remain balanced. Debits and credits are the instruments by which this balance is maintained, thereby preventing errors and ensuring that the company's financial position is accurately reflected.

Question 4: What are common examples of transactions where debits and credits are used?

Numerous transactions utilize debits and credits. For instance, when a company purchases supplies with cash, the supplies account (asset) is debited, and the cash account (asset) is credited. When services are performed for cash, the cash account (asset) is debited, and the revenue account (equity) is credited. These are just a few examples, highlighting the diverse applications of these accounting tools.

Question 5: What are the potential consequences of incorrect debit/credit entries?

Errors in debit and credit entries can lead to significant inaccuracies in financial statements, misrepresenting the company's financial position. This misrepresentation can impact decisions made by stakeholders (investors, creditors, management), potentially leading to incorrect estimations and potentially poor strategic choices. Consistent and accurate recording is critical for maintaining reliable financial information.

Understanding the fundamental principles of debits and credits is crucial for maintaining accurate financial records and facilitating sound decision-making.

Next, we will explore the practical application of these principles through specific examples.

Conclusion

The concepts of debit and credit are fundamental to accurate financial record-keeping. Double-entry bookkeeping, built upon these principles, ensures that the accounting equation remains balanced. This fundamental balance is essential for reliable financial reporting, a crucial component of effective business management. The consistent application of debits and credits, when correctly applied to various account types assets, liabilities, equity, revenue, and expenses allows for an accurate representation of a company's financial position and performance. This framework enables informed decision-making, strategic planning, and ultimately, a comprehensive understanding of a business's financial health.

The meticulous application of debit and credit principles ensures the reliability of financial statements. Accurate and consistent recording of financial transactions, meticulously following the rules governing debits and credits, fosters trust among stakeholders, including investors, creditors, and management. This fundamental understanding is essential for any individual navigating the complexities of financial accounting. Adherence to these principles underscores the importance of maintaining accurate and trustworthy financial records for informed decision-making and responsible financial management.

You Might Also Like

Offspring Lead Singer Death - Shocking NewsIYKYK Dispensary: Your Cannabis Hub!

MV80W: Top Features & Reviews

Kim Stevens At WDRB: Latest News & Updates

Drake's Second Child: Everything We Know

Article Recommendations

- Bill Emerson Bridge History Facts

- 1955 Quarter Value How Much Is Your Coin Worth

- Best Led Qr Codes For Your Project Display